project Betfair, part 3

Table of Contents

Introduction

Previously on project Betfair, we started collecting dumps of Betfair order book data from the Stream API and learned how to reconstruct series of events from those with the aim of using them to backtest a market making strategy.

Today, things get messy.

Insights into the data

As a market maker, our main source of profit should be our orders getting matched, and not us having a directional view (as in betting on which way the odds will move). Hence it's worth investigating how volumes of matched bets vary as the beginning of the race approaches.

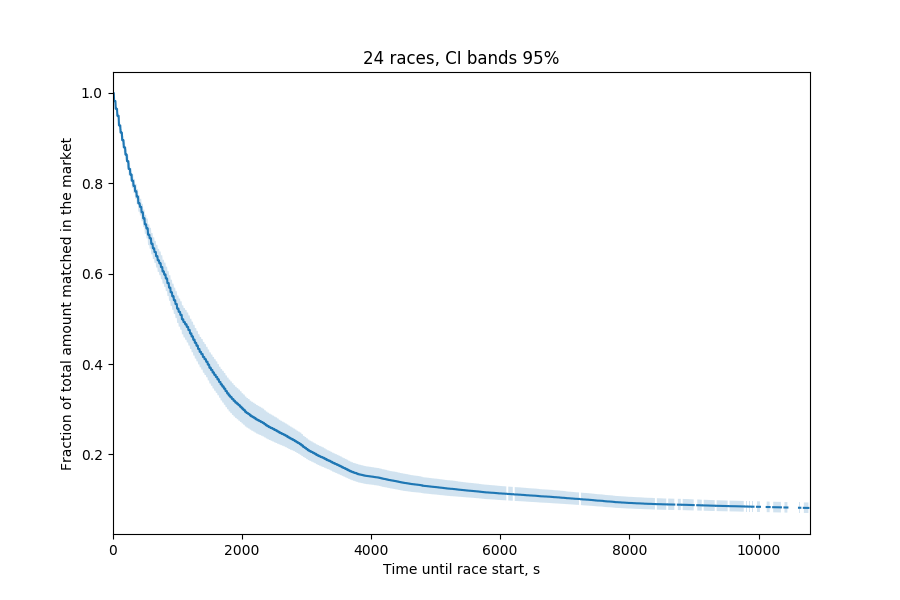

Total matched volume

I took the total bet volumes matched on each race through time, starting from 3 hours before the race, and normalized them by diving by the final total volume just before the scheduled race start time (essentially getting the cumulative fractions of the total matched volumes). There are 24 races in this dataset: I now have quite a few more, but their recording is started much closer to the kick-off, and you'll soon see why.

As you can see, bet matching in pre-race horse trading follows a power law. About half of the total bet volume is matched 10 minutes before the race begins, and 80% of all betting happens within 50 minutes from the race start. Note this doesn't include in-play betting where I guess this gets even more dramatic.

Hence there's not much point doing market making earlier than about 15 minutes before the race. Or perhaps could it be that the reason nobody is trading is that the costs are too high?

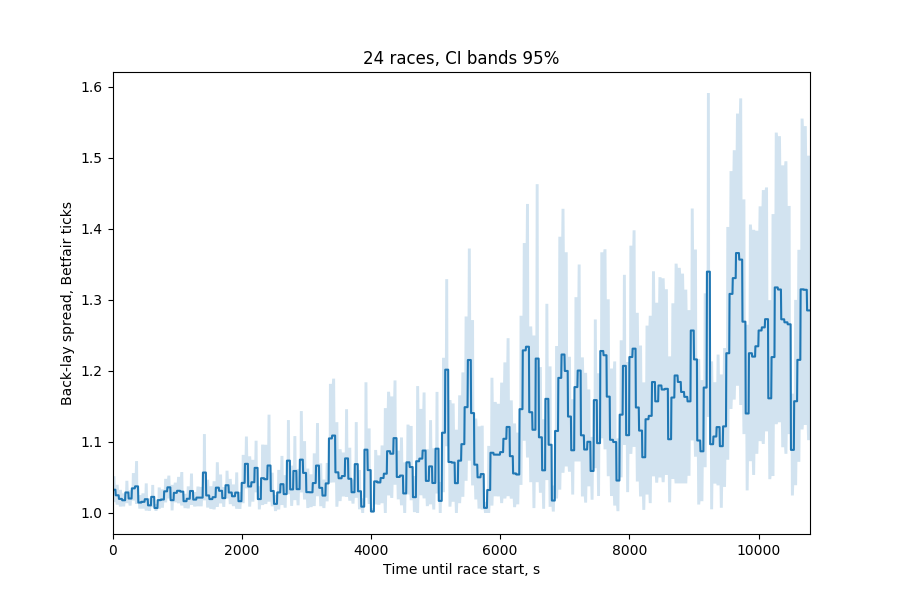

Back-lay spreads

I plotted the average back-lay spreads through time, and it doesn't seem so. The spreads here are in Betfair ticks: the smallest one is 1 (corresponding to, say, best available back odds of 1.72 and best lay odds of 1.73, or best back at 2.50 and best lay at 2.52). Even 3 hours before the race begins, the spreads, on average, are as tight as they can be.

Design

One useful thing about way the Betfair Stream API is designed is that with the tools given to us, we can maintain a state of the order book in our program as well as our own orders. It's essentially like having the data from API-NG available to us at all times, with notifications when it gets updated.

I decided to split the market-making bot into two parts.

The core would be given the current state of the order book and output the amount of one-pound contracts that it wanted to be offering at both sides of the book, together with the odds. The core's operation would be independent of what's happening to our outstanding orders: if we already have a back bet in the book and the core of the strategy wants to be offering the same amount, then no actions would be produced.

Reconciling the core's wishes with the actual state of our orders would be the execution harness' job. Given the desired offers we wish to maintain on both sides of the book and the state of our orders, it would produce a sequence of cancellations and order placements and submit them to Betfair.

Since all of these inputs (the state of the order book and all of our orders) are actually given to us by the Betfair Stream API, this has a neat bonus of behaving in a consistent way if the bot, say, crashes: we can just start it up again and the API will helpfully give us back all our outstanding orders and positions (not that it's a good idea to blindly trust it). Polling the strategy to find out what actions it wants to perform can be done at any point in time: on a schedule or, say, whenever a new event arrives from the Betfair stream.

So the whole strategy would look something like this:

- When a new event arrives:

- Incorporate it into our cached state of the order book and our orders (Betfair even have a guide here).

- Give the order book to the core, request the amount of contracts it wants to offer and the odds (prices).

- On both sides of the book, compare our current outstanding orders and what the core wants to do. For every price level, if what the core wants to offer is different from what we are offering with our outstanding orders:

- If the core wants to offer more, submit an order placement for the difference.

- If the core wants to offer less, take a list of our outstanding orders at that price level (since there might be several) and start cancelling them, newest first (since they're the least likely to get matched) until we reach the desired volume.

There are some operational issues with this (such as Betfair not usually allowing bet placements below £2), but this is a good general platform to build upon and definitely good enough to start simulating.

Backtester

With an order book simulator already built, augmenting it to inject strategy events is fairly easy. Let's say the simulator operates by maintaining a timestamped event queue (where the events are either placing a bet or cancelling one). We add another event type at given intervals of time (say, 100ms): when the backtester sees it, it gives the current order book and the state of the strategy's orders to the strategy, gets its actions from it and then inserts them back into the queue.

To simulate the delay between us and the exchange, the events are timestamped slightly into the future (say, 75ms) so the simulator might not get to apply player orders to the book immediately and may have to handle other orders before that.

In addition, I got the backtester to record various diagnostics about the strategy every time it polled it, such as how many contracts (actually matched bets) it owned, when its orders got matched and whether the matches were passive (initiated by someone else) or aggressive (initiated by the strategy) etc.

Meet CAFBot

There will also be a DAFBot at some point. This was a very early version. It's fairly different to what I actually ran to make the following plots, but the general idea is the same. I also moved the whole codebase to using integer penny amounts instead of floats soon after this commit.

Overview

It was time to find something to plug into the backtester. I decided to first go with the most naive approach: the core would look at the current best back and lay offers and then offer 10 one-pound contracts (recall that this results in a bet of £10 / odds) on both sides.

Since the execution harness compares the desired offers with the current outstanding bets, that would mean when the strategy was started, it would first place those two bets and then do nothing until at least one of them got fully or partialy matched, at which point it would add back to the bet to maintain the desired amount. If the market were to move (the best back/lay offers changed), the strategy would cancel the orders and replace them at the new best bid/offer.

Finally, 15 seconds before the race start, the strategy would aggressively unload its accumulated exposure (say, if more of its back bets were matched than the lay bets) by crossing the spread (and not waiting to get matched passively).

In terms of markets, I would simulate it from 1 hour before the beginning of the race, running it only on the favourite horse (the one with the lowest odds at that point).

With that in mind, I managed (after a few days of debugging) to simulate it on a few races. So, how did it do?

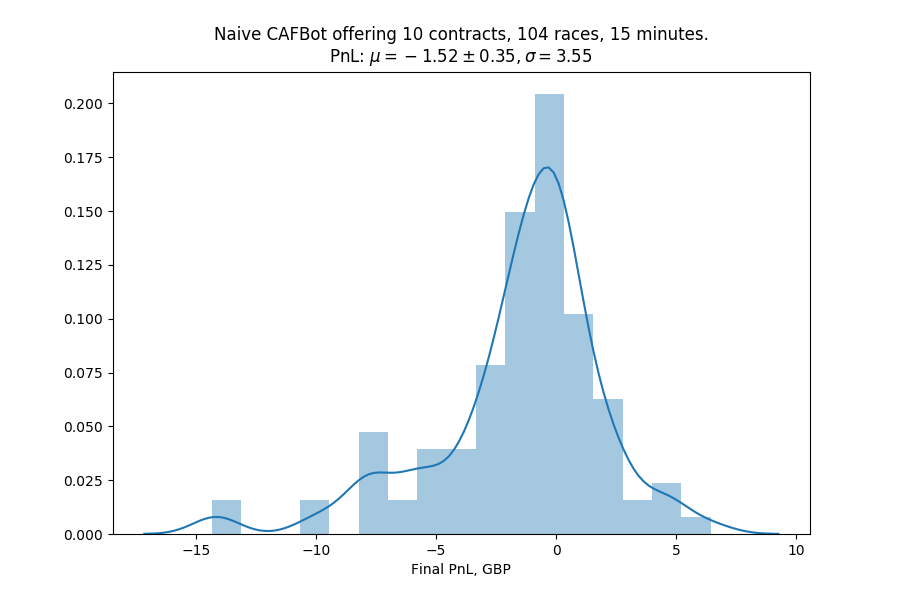

Backtest results

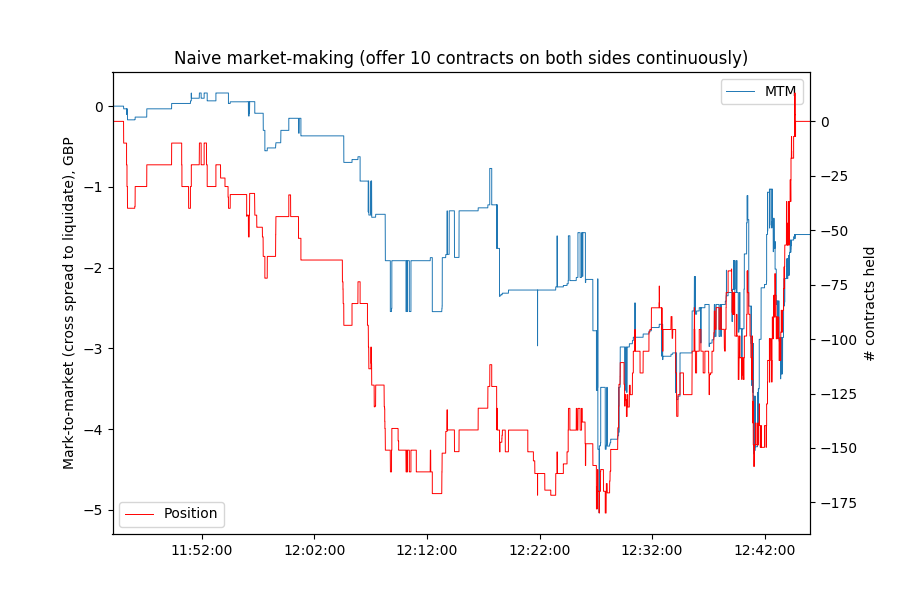

Here's a result from one race:

Well, this is not looking great.

To explain that plot, the red line is the strategy inventory, or position: how many one-pound contracts it's currently holding. For example, with a position of -170, the strategy will lose £170 if the runner we're trading wins (and £0 if it loses, but in any case we get to keep the money we got from selling the contract). The blue line is the mark-to-market of the strategy: how much money we would make/lose if we were to liquidate our position immediately by crossing the spread, like we do in the last 15 seconds before the race begins.

This is obviously just one race, but surely with an HFT strategy we would expect more consistent profit even within one race? For example, Greg Laughlin of the WSJ did a small investigation into the trading of Virtu, an HFT firm, from their abandoned IPO filings, and showed that with a 51% percentage of profitable trades and about 3 million trades a day their chance of having a losing day was negligible.

But we're not making that many trades here and so perhaps this could be a statistical fluke. It's a good thing I now have all the other race data, collected during further experiments, to check this against.

Nope. Running this against 104 races (albeit with 15 minutes of trading, since the latter datasets I collected were shorter), we can see that the bot has systematic issues and loses, on average, £1.52 per race.

So what happened in the first plot? It looks like we had a fairly chunky short exposure (betting against) throughout the trading. At its worst we were short 175 contracts, which is 17 times more than what we were offering to trade. So there was an imbalance in terms of which side of our offering was getting executed.

Investigating further...

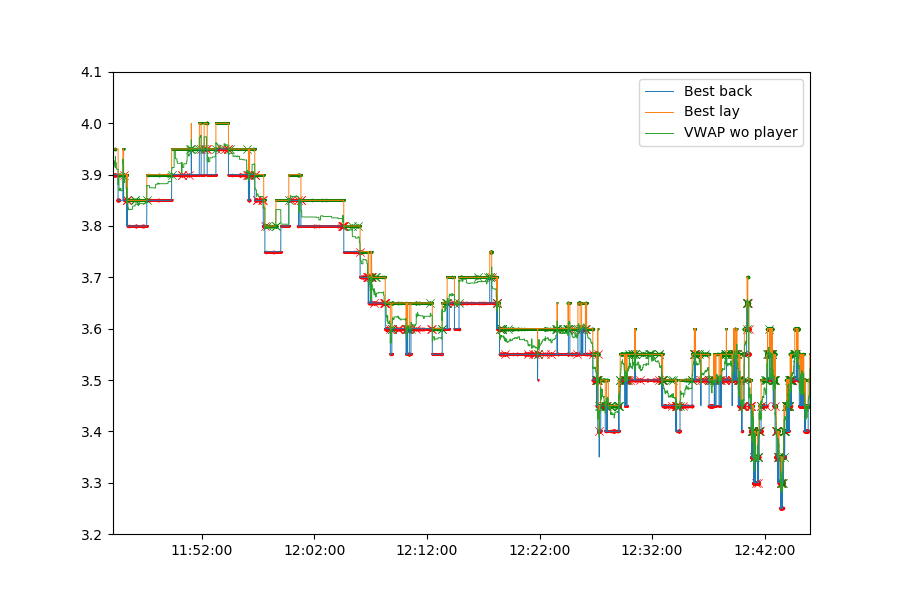

As you can see from the odds plot, the price of the contract (inverse of the odds) trended upwards throughout the final hour before the race, with a few range-bound moves closer to the start. That explains us losing money and also kind of explains us selling too many contracts: in a trending market, there would be more matching on one side of the book, hence a naive strategy that doesn't account for that would quickly get out of balance. Or at least that's what it looks like. There are many ways to read this.

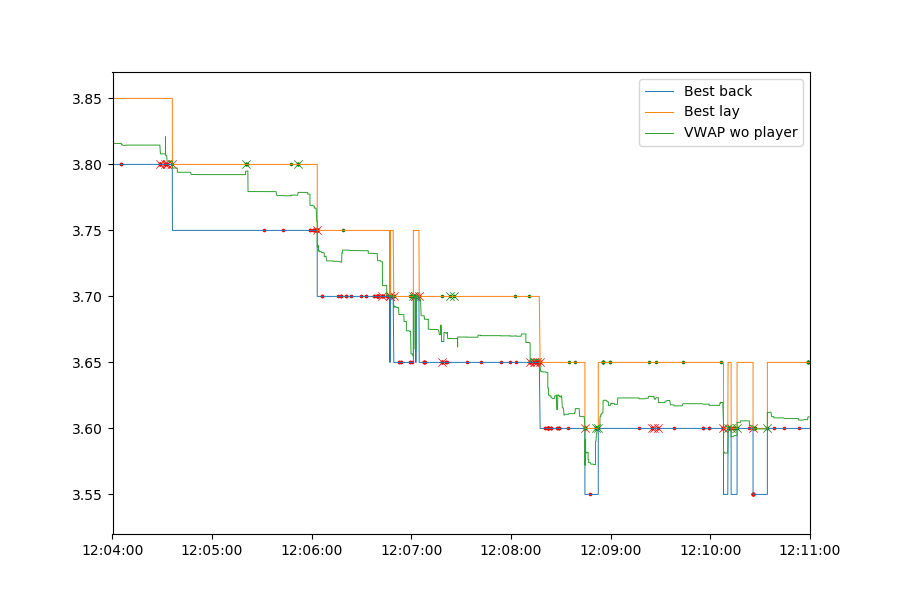

This is the previous plot, but zoomed in towards the part where we lost money the fastest. The orange line shows the best available lay odds and the blue one is the back odds (both of which are where our simulated bot also puts its bets).

The green line in the middle is the volume-weighted average price, or the microprice. It's calculated as follows:

\[ \text{VWAP} = \frac{\text{BBPrice} \times \text{BLVolume} + \text{BLPrice} \times \text{BBVolume}}{\text{BBVolume} + \text{BLVolume}} \]

Essentially, if the volume of available bets on one side is bigger, then that side kind of pushes the microprice towards the opposite side. It's a good way to visualize order book imbalance and, interestingly, in that plot, sometimes a move in the actual best back/lay odds can be anticipated by the microprice moving towards one side or the other. We'll look into that later.

The crosses are the bot's orders getting executed: red means the back offer got executed (thus the bot has secured a lay bet and is now more short the market) and green means the lay offer got executed. The dots are the same, but for other people's orders.

What's strange here is that our orders often get hit shortly before there's a price move against us: for example, in the beginning, just before the best back moves from 3.80 down to 3.75 (this is still a 1-tick move), you can see several executions of the bot's back orders, with the bot quickly replacing them several times in between executions. In essence, it's sort of trying to "hold the line" against a market move, but ultimately fails and ends up with having bet against the market whilst the odds managed to move through it. Well, at least we know it's a market move in hindsight: perhaps more people could have joined the bot on its side and maintained the price.

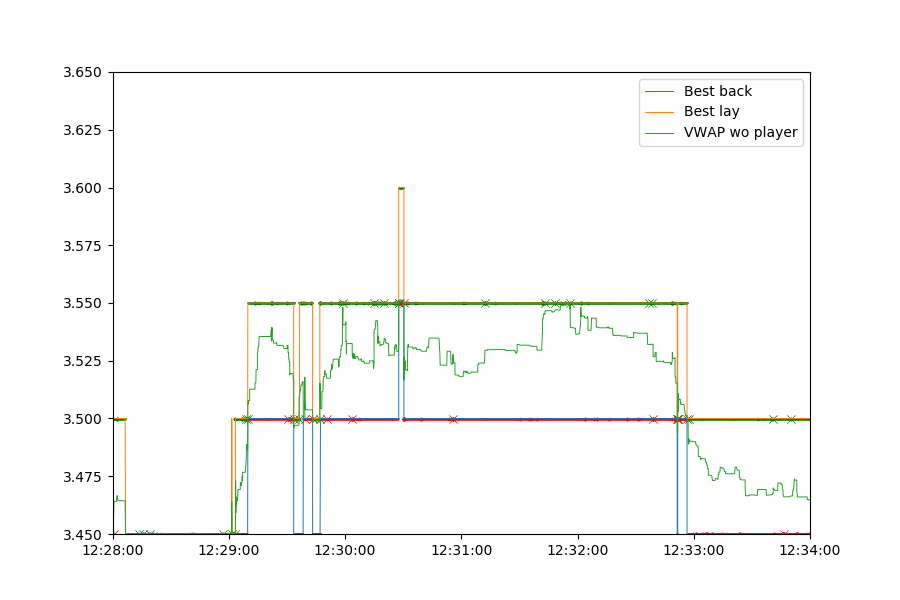

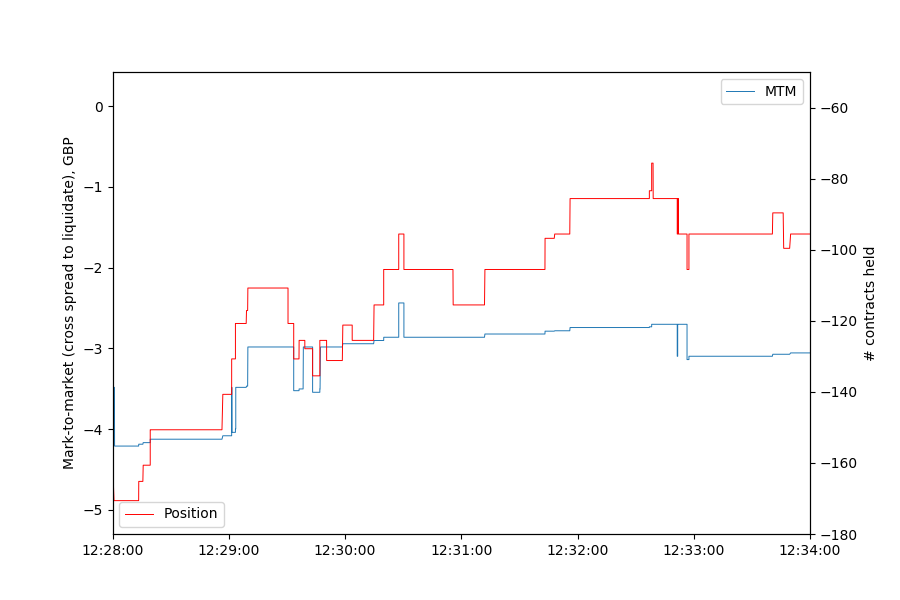

Essentially, the bot does well during times when there's a lot of matching going on on both sides of the book and the price isn't moving. This happens, for example, for a few minutes around 12:30:

But even in this case, this doesn't look too inspiring: the initial 1-pound jump in the PnL at 12:29 is because of the odds moving up and us having a short exposure. The actual market-making part between 12:29 and 12:33 only makes about £0.10.

So in the end, looks like it's back to the drawing board.

Conclusion

Not all was lost, obviously. I had a backtesting engine, a half-working strategy (in that it didn't immediately start bleeding money) and I had an idea of what was going wrong and some possible ways to fix it. And obviously no real money had suffered yet in the making of this.

Next time on project Betfair, we'll start reading some actual papers on market making and tinkering with the bot in attempts to make it lose less money. Perhaps I'll tell about what was happening to the Scala version (that would later supposedly be a production version of this thing) as well. Stay tuned!

As usual, posts in this series will be available at https://kimonote.com/@mildbyte:betfair or on this RSS feed. Alternatively, follow me on twitter.com/mildbyte.

Interested in this blogging platform? It's called Kimonote, it focuses on minimalism, ease of navigation and control over what content a user follows. Try the demo here and/or follow it on Twitter as well at twitter.com/kimonote!